Top 3 Personal Finance Mistakes Women Commonly Make (+ How To Avoid These)

Credit: Nick Noel

Do you find yourself walking into the proverbial wall every time you try to make a financial decision? You’re not alone. Here are common financial mistakes women make and some suggestions on how to overcome these hurdles.

According to the OCBC Financial Wellness Index 2020, women consistently fared worse than men in planning for their retirement (58% women started planning vs 68% men), having investments (60% women investors vs 75% men) and feeling confident and knowledgeable about investments (28% women vs 48% men).

As a woman in the financial sector, this number made me feel anxious, yet I wasn’t surprised. It bears out the trend that I’ve observed myself among my women clients and strengthens my resolve to educate and empower women to be confident and independent with their finances.

Here, I’d like to highlight the top three mistakes I commonly observe, and how you can move past them to start taking control of your financial destiny.

1. Putting Someone Else In Charge of Your Finances

Many women prefer to have someone else take care of their finances - whether it’s their parents, spouses, or older children. Women tend to entrust someone else to plan and manage their finances.

But what if your relationship or marriage doesn’t work out? What if your father manages your bank accounts and he passes on unexpectedly, or your siblings or children fight for your share?

The issue with putting someone else completely in charge of your finances is this: you lack control of your money. You may feel secure by having them manage it but if you don’t know anything about it, that might be a problem in the future.

Take a real story that happened to someone close to me: April (not her real name) gave her entire salary to her husband every month as she was too busy with her job whereas he was always on the lookout for investment opportunities. It was only when they started receiving demand letters from the banks that she realised her husband had over-leveraged on mortgage loans to buy multiple properties, even re-mortgaging their marital house which she always thought was fully paid up. He dreamed of collecting rentals from multiple properties that they can eventually pass on to their two children. Instead, they were left without savings and no house to call their own. Sadly, their marriage did not last long after this.

Let your spouse, parent, or child be aware of your financial health but don’t give them full control of it. If you choose to let a family member make financial decisions on your behalf, at least make sure that all transactions are done with your full knowledge and blessing. I also encourage all women to engage a professional financial adviser who can lend an impartial lens to sensitive and emotional money, and by extension, family issues.

2. Being Too Conservative With Money

Women tend to be geared towards security and stability. The pain of losing money hurts much more than the pleasure of making good returns. Coupled with a tendency to think less of their own ability (I’m generalising here - if you’re not like that, good for you!), women tend to prefer savings accounts, fixed deposits and insurance endowment plans that provide “guaranteed” returns.

However, in today’s low-interest rates environment, even financial institutions are finding it difficult to maintain the promised returns. Our local banks announced multiple rate cuts last year. This year, insurers also announced a downward revision of projected returns. You don’t need to look at statistics to know instinctively that the returns you get on such “guaranteed” products are not even on par with inflation. So since you’re already losing money to inflation, why not take it one step further and invest in something that can provide you with more gains in the long run, that actually has a reasonable expectation of helping you reach your financial goals?

There are many free tools out there to help you get started. Type investing into YouTube and you’ll get lots of videos from investors sharing how they did it. You can pay some money to attend courses by successful investors, or if you'd rather skip the work, you can check out the many Robo advisory platforms, or seek the help of a professional financial adviser. (Pro tip: ask the adviser how he/she’s remunerated - you want someone whose interests are aligned to yours. Bonus if they can share through their own investment experience.) Whatever you choose, know that markets always trend upwards in the long run, and it’s to your advantage to get in early.

3. Delaying Crucial Financial Decisions

Too busy with work? Concentrating on family planning? Hands tied with caring for elderly parents or young kids?

These are some of the many reasons why women end up delaying crucial financial decisions. They tend to have their hands and time so full with managing other daily affairs that they don’t have time to sit down and plan their finances.

Here’s an illustration of just how much more you need to invest when you delay your action plan:

In the above scenarios, you can see that investing early will cost you much less, and potentially gain you more with a principled, well-planned investment portfolio.

One of the things you should also know when it comes to investing is risk management. It’s a big part of investing well, and one of the best risk management tools for your life is to get life and health insurance. Think of it as securing your defences before you go into a more volatile environment like stocks. When you get health insurance at a younger age, you pay less premium. The longer you wait, the higher the risk of your health deteriorating to the extent where you may face a “loading” where you have to pay an extra premium, “exclusion” where you won’t be able to claim for pre-existing illnesses, or even an outright decline.

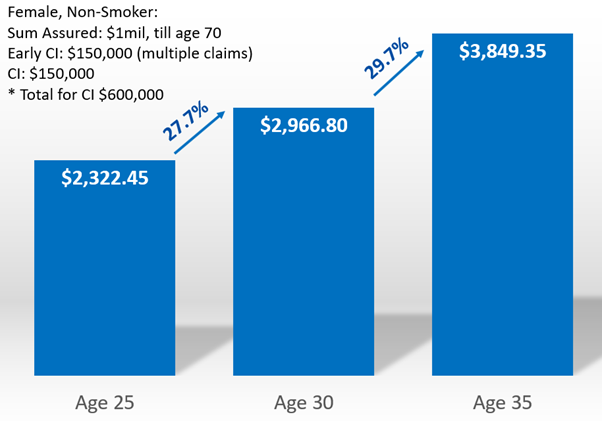

Here’s another chart to demonstrate the benefit of securing life and health insurance for yourself at a much earlier age.

In this world of information overload, a seemingly simple decision to buy health or life insurance or saving for retirement can lead to women being overwhelmed with options and end up with “analysis paralysis”. This is why many women just sweep these decisions under the carpet until something happens (like a health scare, or hitting the big 40), and by then it just might be a little too late in the game.

Just as companies have to report their finances every year, we too should set aside time to review our finances at least once a year. Pick a time that’s easy for you to remember, like when it’s time for your work review, when you get your bonus or your birthday.

Women, after all, have a life expectancy that is five years more than men (in Singapore, at least), and we need to have our finances sorted out to ensure we can continue living a comfortable life after retirement and if we’re alone in old age. Your parents could also still be living and in need of your support!

If you have any concerns about how to manage your finances or know someone who could use some sound advice, drop me a note. Let’s get in touch.

This page is purely for informational purposes only and should not be relied upon as financial advice. The statements and opinions expressed on this page are my own and are not endorsed by finexis.